Making Capital Expenditure Decisions During Times of Uncertainty, e.g., COVID-19

If you are an owner or manager of a business, you are likely an operator and an investor. As an investor, you decide what to do with the capital you have. Should you: 1) keep it in cash, 2) reinvest in your business or 3) return it to shareholders? Alongside day-to-day management, deciding what to do with the capital available to you drives the success of your business. Consider this quote from Warren Buffett:

The lack of skill that many CEOs have at capital allocation is no small matter: After 10 years on the job, a CEO whose company annually retains earnings equal to 10% of net worth will have been responsible for the deployment of more than 60% of all the capital at work in the business.

Your investment decisions today will determine your success tomorrow. Our goal in writing this article is to begin a discussion on how our industry can evaluate capital expenditure decisions during times of uncertainty.

Uncertainty

Uncertainty

For the past few months we have discussed COVID-19, but before COVID-19 we had tariffs, healthcare policy, tax policy, the 2016 election and the upcoming 2020 election all threatening to change the business environment. The future for business is rarely clear. So, what should you do when you are not sure what the future holds? How do you decide whether to go forward with a planned investment when COVID-19 strikes?

We posit three categories to consider before making a capital expenditure decision during times of uncertainty:

- Technicals: Know your numbers.

- Emotion: Understand yourself.

- Tools: Apply technicals and limit the impact of your emotions.

Technicals

The first step in making wise investment decisions is understanding your cost of capital and return on invested capital (ROIC). That is, how much does it cost you to use debt and/or equity capital? And how much do you earn by using that capital? An investment is only worthwhile if your ROIC is greater than your cost of capital. Understanding these numbers will help you make wise — and timely — capital expenditure decisions.

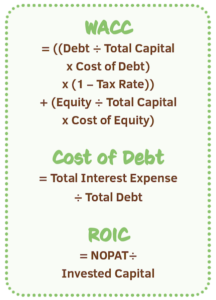

Your cost of capital is determined by your capital structure, which is the mix of debt and equity your company employs. Therefore, you can determine your cost of capital by determining your cost of debt and cost of equity, then weighting those costs by the percentage of debt versus equity employed by your business. The formula used to do this is called the Weighted Average Cost of Capital (WACC).

Your cost of capital is determined by your capital structure, which is the mix of debt and equity your company employs. Therefore, you can determine your cost of capital by determining your cost of debt and cost of equity, then weighting those costs by the percentage of debt versus equity employed by your business. The formula used to do this is called the Weighted Average Cost of Capital (WACC).

If you know your cost of debt and cost of equity, calculating your WACC is simple. The formulas for determining your cost of debt and cost of equity depend on whether your company’s debt and equity is private or public. For this exercise, we will assume both debt and equity are private. To determine your cost of debt, divide your total interest expense by your total debt.

Determining your cost of equity is more complicated. For public companies, the cost of equity is estimated using the capital asset pricing model (CAPM). Private companies can adjust the CAPM to determine their cost of equity but we suggest using an alternative approach.

Think about your cost of equity as the return required for you to invest in your business. For example, if you expected a 5% return on equity you invested in your business, would you invest? What if you expected a 10% return? How about 15%? The return at which you say, “Yes, I would invest” is your cost of equity. If your business has multiple equity investors, you also need to determine the return at which they would invest.

After calculating your WACC, you need to determine your ROIC. To do this, divide net operating profits after tax (NOPAT) by invested capital. If your resulting ROIC is greater than your WACC, the investment is worth considering.

Other factors that must be considered are cash on hand, cash burn rate, the option value of money and operating leverage.

Emotions

As an investor, it is important to understand yourself: Are you risk averse? Are you impulsive? Are you an optimist or a pessimist? How much weight do you give your emotions when making decisions?

Understanding yourself decreases the likelihood you will make decisions affected by biases and heuristics. Biases are preconceived opinions toward something. Heuristics are mental shortcuts that increase expediency but also increase risk of error.

Most people are at greater risk of introducing biases and heuristics into their decision-making during times of uncertainty. To avoid this, we recommend discussing your decisions with people who are objective, believable and may have contrasting views.

Tools

Conventional methods used to evaluate investment decisions include, Internal Rate of Return (IRR), Accounting Rate of Return (ARR), Payback Period, Net Present Value (NPV) and Expected Value with Decision Trees. Two methods we recommend when making your next capital investment decision are a variation of NPV and Expected Value with Decision Trees. Completing these analyses will help you thoroughly consider the investment.

Net Present Value: This analysis was introduced in America in 1907 and has been widely adopted by investment professionals. NPV works by forecasting cash flows and discounting them to the present.

NPV is an attractive approach because it accounts for the time value of money and provides a single number on which to base your decision. The primary challenge with every NPV analysis is forecasting cash flows. Variations of the NPV approach seek to control for this by running “what-if” analyses, called

Monte Carlo Simulations. By running hundreds, sometimes thousands, of simulations, you get a better idea of possible outcomes and the probability of those outcomes occurring. While this variation greatly improves the traditional NPV approach it does not control for the option value of money.

Expected Value with Decision Trees: While the NPV approach is binary — to invest or not to invest — the Expected Value with Decision Trees considers multiple options. A classic use-case is buy versus build scenarios. In our industry, this might be the decision to fulfill increasing demand with contract growers versus building additional acreage. A third option might be to choose a combination thereof.

This approach accounts for the option value of money by applying probabilities to the event of various possible scenarios. In the previous example, we might determine that the likelihood of increased demand remaining for more than 10 years 60% and the likelihood of it remaining for 10 years or less is 40%. The analysis might look something like the figure above.

In this simple example, the expected value of contract growing versus building is the same. If these were the only options, either choice would be justifiable. In this case, however, the combination of contract growing and building results in the highest expected value and should, therefore, be chosen.

Conclusion

At our company, Silver Fern Group, we recently applied these exercises to make a capital expenditure decision in the heart of COVID-19 and it saved us 30% on our up-front cost. By knowing our numbers (Technicals), understanding ourselves (Emotions) and using Tools, we were able to think beyond the pressures caused by uncertainty and move forward with our capital expenditure decision. If you found this helpful, or would like to discuss further, please connect with us at www.silverferngroup.com.

Video Library

Video Library